Finding Relative Tariff Winners

Who is ahead of their peers when it comes to handling the tariff fall-out?

You didn’t need a Bloomberg terminal yesterday to figure out that there was more than a bit of indiscriminate selling pressure in the market.

Days like this with heavy technical selling, while painful, open the door to a classic value investment mental model: finding the “baby thrown out with the bathwater”. The concept is exactly what it sounds like; if equities are being sold as a basket, there are likely some higher quality companies that are unfairly being lumped in with the masses.

That said, the current situation is nuanced. Of course, there’s the very real risk of a recession; the heatmap above certainly reads like a market knee-jerk repricing of a cyclical downturn. But also at play are the complex distortions introduced by these new tariffs at the microeconomic company level; what happens to any given company assuming a certain level of US and retaliatory international tariffs?

Forecasting the macro implications of a development we haven’t seen in ~100 years (and even then, Smoot-Hawley was implemented in a far less globalized world) is beyond the scope of this post. However, a far more researchable question is which companies may be relatively better positioned to handle a high-tariff environment than their peers. For instance, companies who already have a domestic supply chain, while their peers rely on offshore manufacturing, are going to be relatively insulated (and may even be able to take advantage of the environment).

Turning to Portrait, here is a sampling of companies whose management teams have argued they are relatively well-positioned to handle tariffs.

The rest of this post is written by Portrait, which surfaced dozens of companies that could be fits. To dig into any of these names, sign up for a demo and trial at portraitanalytics.ai

Camping World Holdings: Positioned to Navigate US Trade Tariffs

Thesis Summary

Camping World Holdings (CWH) is well-positioned to navigate and potentially benefit from US trade tariffs due to its scale advantages, strategic supplier relationships, and focus on private label/contract manufacturing, which collectively provide pricing advantages and supply chain flexibility relative to competitors. While the company does have some international sourcing exposure, its dominant market position, financial strength, and strategic inventory management create a competitive advantage that would likely allow it to outperform peers in a high-tariff environment.

Key Supporting Evidence

Scale and Purchasing Power Advantage

Camping World's significant market share and purchasing power create a substantial competitive advantage that would help mitigate tariff impacts. The company has achieved record market share of 11.2% in the combined new and used RV market as of late 2024, with targets to reach 12% in 2025 and 15% longer-term (Q4 2024 Earnings Call). This scale provides CWH with superior pricing leverage with suppliers compared to smaller competitors. Management explicitly acknowledges this advantage, stating: "Our company does not operate on a level playing field. We do not buy RVs for the same price as everybody else... if tariffs continue to be a problem, they're a problem for everybody, but we tend to enjoy a different level of pricing than everybody else" (Q4 2024 Earnings Call).

The company's market position is particularly strong in the used vehicle segment, where it commands approximately 20% market share (CWH 8-K 01/14/25). This is strategically important in a tariff environment as used vehicles would not be directly impacted by import tariffs on new components. Management recognizes this advantage, noting that "if the tariffs do happen, [used inventory] is only going to become more important to our business" (Q4 2024 Earnings Call).

Private Label and Contract Manufacturing Strategy

Camping World has strategically positioned itself to have greater control over its supply chain through extensive use of private label and contract manufacturing arrangements. Approximately 36% of CWH's new unit sales come from contract manufactured RVs that are exclusive to Camping World, produced through partnerships with Thor Industries and Forest River (Q3 2024 Earnings Call). This approach gives the company more direct influence over product specifications, pricing, and potentially the sourcing of components.

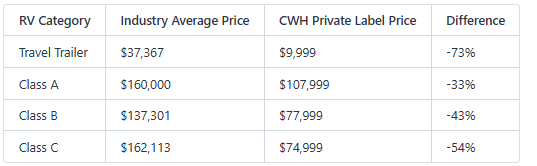

The company has leveraged these relationships to introduce targeted private label units at significantly lower price points than industry averages. For example, while the industry average retail price for travel trailers was $37,367 in late 2024, CWH offered private label alternatives starting at $9,999 (CWH 8-K 01/14/25). Similar price advantages exist across other RV categories:

This focus on affordability is particularly important in a tariff environment, as it gives CWH more flexibility to absorb or pass on cost increases while still maintaining competitive pricing. Management has indicated they are "frankly okay with" potential 3% price increases due to tariffs, suggesting confidence in their ability to manage through such impacts (Q4 2024 Earnings Call).

Strong Financial Position and Inventory Management

Camping World has taken proactive steps to strengthen its financial position and manage inventory in ways that would provide advantages in a tariff environment. In October 2024, the company raised approximately $288.8 million in a public offering to strengthen its balance sheet (CWH 8-K 10/30/24). Additionally, in February 2025, CWH amended and extended its floor plan facility, increasing it from $1.85 billion to $2.15 billion (CWH 8-K 02/19/25).

This financial flexibility is complemented by strategic inventory management. Management has noted that their current inventory "is devoid of some of those potential tariffs" (Q4 2024 Earnings Call), suggesting they have positioned their stock ahead of potential tariff implementation. The company has also been disciplined in managing its used inventory levels, which would be less affected by tariffs on imported components.

While CWH does have some international sourcing exposure, it appears relatively limited compared to the company's overall cost structure. In 2024, directly sourced inventory from China, Mexico, and Canada totaled approximately $39 million combined (CWH 10-K FY 2024), a small fraction of the company's total inventory of over $1.8 billion as of December 31, 2024 (CWH 8-K 02/25/25).

Camping World's financial strength and inventory positioning, combined with its scale advantages and private label strategy, make it well-equipped to navigate and potentially benefit from a high-tariff environment relative to its competitors in the RV industry.

Business Description

Camping World Holdings, Inc. (CWH) is the world's largest retailer of recreational vehicles (RVs) and related products and services. The company operates through two main segments: Good Sam Services and Plans, and RV and Outdoor Retail. CWH offers a comprehensive assortment of RV products and services, including new and used RV sales, financing, insurance, repair, maintenance, and installation of RV parts and accessories. The Good Sam segment provides extended vehicle service contracts, roadside assistance, property and casualty insurance, travel protection, and access to a network of campgrounds. As of December 31, 2023, CWH operated 202 store locations across the U.S., with a significant online presence and a network of call centers to support customer service. The company focuses on delivering exceptional value and customer service, leveraging its national network and proprietary tools to engage and promote its wide range of products and services.

Ethan Allen Interiors Inc. (ETD): Positioning in a High-Tariff Environment

Thesis Summary

Ethan Allen Interiors Inc. is well-positioned to navigate a high-tariff environment relative to industry peers due to its predominantly North American manufacturing footprint, limited international revenue exposure, and vertically integrated business model that provides operational flexibility to adapt to trade policy changes.

Key Supporting Evidence:

North American Manufacturing Concentration

Ethan Allen manufactures approximately 75% of its furniture products in North American facilities, significantly reducing vulnerability to broad-based import tariffs compared to competitors who rely more heavily on overseas production (Ethan Allen Interiors Inc., Q2 2025 Earnings Call, Jan 29, 2025, ETD 10-Q Q2 2024). The company operates a robust North American manufacturing network consisting of:

Four manufacturing plants, one sawmill, one rough mill, and one kiln dry lumberyard in the United States

Three manufacturing plants in Mexico

One manufacturing plant in Honduras

While the Mexican and Honduran operations would potentially be subject to tariffs in a scenario where the US imposes duties on imports from these countries, management has explicitly addressed this risk with contingency plans. As CEO Farooq Kathwari noted, "There's a possibility that more of that product could be made in North Carolina because we are manufacturing in both places" (Ethan Allen Interiors Inc., Q2 2025 Earnings Call, Jan 29, 2025). This manufacturing flexibility represents a significant competitive advantage in adapting to changing trade policies.

Minimal International Revenue Exposure

Ethan Allen's business is overwhelmingly focused on the domestic US market, with international sales representing only a small fraction of total revenue. According to recent financial reports, international sales accounted for just 1.4% of total wholesale net sales during the second quarter of fiscal 2025, down from 2.0% in the prior year quarter (ETD 10-Q Q2 2024). This limited international exposure means the company would face minimal impact from potential retaliatory tariffs that trading partners might impose on US exports.

The company's retail footprint further demonstrates this domestic focus:

137 company-operated retail design centers in the US

4 company-operated retail design centers in Canada

46 independently owned and operated design centers globally

This predominantly US-based retail network insulates the company from significant cross-border trade disruptions that would more severely impact competitors with greater international sales dependency.

Vertical Integration Provides Adaptability

Ethan Allen's vertically integrated business model—encompassing product design, manufacturing, logistics, and retail—provides significant flexibility to respond to tariff-related challenges. Management has explicitly acknowledged their preparedness for potential tariff scenarios and outlined specific mitigation strategies:

Price Adjustment Capability: "There's a possibility we could consider raising prices" (Ethan Allen Interiors Inc., Q2 2025 Earnings Call, Jan 29, 2025). The company's control over its entire value chain enables more efficient price adjustments compared to companies with fragmented supply chains.

Production Reallocation: The ability to shift production between facilities in different countries provides a hedge against country-specific tariffs. For example, upholstery production currently split between Mexico and North Carolina could be reallocated if tariffs on Mexican imports increase significantly (Ethan Allen Interiors Inc., Q2 2025 Earnings Call, Jan 29, 2025).

Supply Chain Control: "Our national and retail logistics is unique and a great competitive advantage, enabling us to deliver our products with what we say white glove delivery at one cost in North America to our clients" (Ethan Allen Interiors Inc., Q2 2025 Earnings Call, Jan 29, 2025). This logistics network would help maintain service levels even if supply chain disruptions occur due to tariff-related adjustments.

Management has demonstrated awareness of tariff risks, noting in financial filings that "The U.S. President has discussed implementing a 10-20% tariff on U.S. imports, a 25% tariff on imports from Mexico and Canada, and increasing the tariff on Chinese products to at least 60%" (ETD 10-Q Q2 2024). However, they also express confidence in their positioning, stating "We are looking at all the events in the world. And the good news is we are well positioned and we are also positioned to take steps based upon whatever happens and whether it's a question about duties and anything else" (Ethan Allen Interiors Inc., Q2 2025 Earnings Call, Jan 29, 2025).

While Ethan Allen would not be entirely immune to the impacts of broad-based tariffs—particularly on the 25% of products it sources internationally and on raw materials imported for its North American manufacturing—its business model provides significant relative advantages compared to furniture retailers and manufacturers with higher import dependency and less operational flexibility.

Business Description

Ethan Allen Interiors Inc., through its wholly-owned subsidiary Ethan Allen Global, Inc., is a leading interior design company, manufacturer, and retailer in the home furnishings marketplace. The company is a global luxury home fashion brand that is vertically integrated from product design through home delivery, offering customers stylish product offerings, artisanal quality, and personalized service. Ethan Allen operates 139 retail design centers in the U.S. and Canada, with additional independently-operated centers in Asia, the Middle East, and Europe. The company owns and operates ten manufacturing facilities, including plants in the U.S., Mexico, and Honduras, producing approximately 75% of its products in North America. Ethan Allen's business model focuses on providing relevant product offerings, leveraging vertical integration, investing in new technologies, maintaining a strong logistics network, and utilizing its website as a key marketing tool. The company emphasizes quality, craftsmanship, and exceptional personal service, with a commitment to social responsibility and sustainable operations.

Eagle Materials Inc.: Positioned for Advantage in a High-Tariff Environment

Thesis Summary:

Eagle Materials is exceptionally well-positioned to benefit from significant US trade tariffs due to its entirely domestic manufacturing footprint, US-focused revenue streams, and substantial owned raw material reserves. As a leading US manufacturer of essential construction materials with minimal import dependency, the company would likely gain competitive advantages relative to import-reliant competitors facing higher costs under a tariff regime.

Key Supporting Evidence:

Domestic Manufacturing and Supply Chain Integration

Eagle Materials operates a comprehensive network of more than 70 facilities spanning 21 states across the United States, with zero international manufacturing operations (EXP 8-K 01/29/25 Results of Operations and Financial Condition).

The company maintains substantial domestic raw material reserves, owning at least 25 years (and in many instances, more than 50 years) of primary raw materials for each of its cement and wallboard facilities, providing exceptional supply security and cost control advantages (EXP 10-K FY 2024).

Eagle's vertical integration extends from raw material extraction through production and distribution, with strategic limestone quarries positioned adjacent to manufacturing facilities to minimize transportation costs and supply chain vulnerabilities (EXP 10-K FY 2024).

The company is actively expanding its domestic manufacturing capacity through strategic investments, including:

A $430 million modernization and expansion of its Laramie, Wyoming cement plant that will increase capacity by 50% to 1.2 million tons (EXP 8-K 05/17/24 Regulation FD Disclosure)

A new slag cement facility in Houston, Texas with 500,000 tons annual capacity (EXP 8-K 04/09/24 Regulation FD Disclosure)

Acquisition of Bullskin Stone & Lime in Western Pennsylvania for $152.5 million, strengthening its aggregates network (EXP 8-K 12/10/24 Regulation FD Disclosure)

Geographic Insulation from Import Competition

Eagle's strategic focus on the US heartland provides natural protection from import competition: "Our position in the U.S. heartland, away from most import terminals, provides a degree of insulation from coastal imports, given the expense of transporting cement from deep water ports into the heartland regions" (EXP 10-K FY 2024).

The company's cement operations are concentrated in Colorado, Illinois, Kansas, Kentucky, Indiana, Iowa, Missouri, Nebraska, Nevada, Ohio, Oklahoma, Tennessee, and Texas—regions that would be less economically viable for imported products due to inland transportation costs (EXP 10-K FY 2024).

The low value-to-weight ratio of cement limits economical shipping distances, with truck shipments generally limited to a 150-mile radius and rail shipments to 300 miles, creating regional markets that favor domestic producers (EXP 10-K FY 2024).

Domestic Revenue Concentration

Eagle Materials generates 100% of its revenue within the United States, with approximately 65% coming from ten states: Colorado, Illinois, Kansas, Kentucky, Missouri, Nebraska, Nevada, Ohio, Oklahoma, and Texas (EXP 10-K FY 2024).

The company's strategic focus explicitly includes "operating solely in the United States in regionally diverse and attractive markets," eliminating exposure to retaliatory tariffs that could affect companies with international sales (EXP 10-K FY 2024).

Eagle's primary end markets—infrastructure, commercial construction, and residential construction—are predominantly domestic, with public infrastructure accounting for nearly 50% of cement demand (EXP 10-K FY 2024).

Competitive Advantage in a Tariff Environment

In a high-tariff scenario, Eagle would likely gain market share from the 22% of US cement consumption currently served by imports, as noted by the USGS for calendar 2023 (EXP 10-K FY 2024).

The company's consistent focus on maintaining a low-cost producer position (30.7% gross margins in Q1 2025) provides financial flexibility to navigate any tariff-related disruptions while potentially capturing market share from higher-cost import-dependent competitors (EXP 8-K 07/30/24 Results of Operations and Financial Condition).

Eagle's strong balance sheet (net debt-to-EBITDA ratio of 1.2x as of Q3 2025) and robust cash flow generation ($486 million operating cash flow for nine months ended December 2024) provide substantial financial resilience to weather any temporary disruptions while capitalizing on strategic opportunities (Eagle Materials Inc., Q3 2025 Earnings Call, Jan 29, 2025).

The company's recycled paperboard operations utilize domestically sourced recycled materials (OCC - Old Corrugated Containers), further insulating this segment from potential import disruptions (EXP 10-Q Q3 2024).

Eagle Materials represents an ideal candidate for investors seeking companies that would benefit from significant US trade tariffs. Its entirely domestic operational footprint, substantial raw material reserves, strategic heartland positioning, and strong financial position would likely translate to competitive advantages as import-dependent competitors face higher costs and supply chain disruptions. The company's ongoing investments in domestic manufacturing capacity further strengthen its positioning to capitalize on a potential shift toward domestic sourcing in a high-tariff environment.

Business Description

Eagle Materials Inc. (EXP) is a leading U.S. manufacturer of heavy construction materials and light building materials. The company operates through two main sectors: Heavy Materials, which includes Cement and Concrete and Aggregates segments, and Light Materials, which includes Gypsum Wallboard and Recycled Paperboard segments. EXP's primary products, portland cement and gypsum wallboard, are essential for commercial and residential construction, public infrastructure projects, and repair and remodel activities. The company benefits from strategically located plants, substantial raw material reserves, and a low-cost producer position. EXP also focuses on sustainable practices and has a decentralized operating structure to enhance regional market familiarity and reduce transportation costs. The company has a significant presence in high-growth U.S. markets and continues to pursue growth through acquisitions and organic development.