Portrait Weekly Framing: China & Declining American Auto Competitiveness

Welcome to this week’s edition of the Portrait Weekly Framing. Today, we’ll be diving into how American car companies are losing the market share battle in China.

As Chinese car manufacturers continue to make a name for themselves, American car companies increasingly find themselves in a difficult position. Specifically, the leading candidate for Stellantis’ CEO role said he was “shocked” at the pace at which non-Chinese car manufacturers are losing share in China, according to a FT report.

Notably, the only meaningful market share left for non-Chinese competitors in China is amongst ICE vehicles, not EVs. As ICE phases out, these companies may be looking at a segment / business segment with zero terminal value.

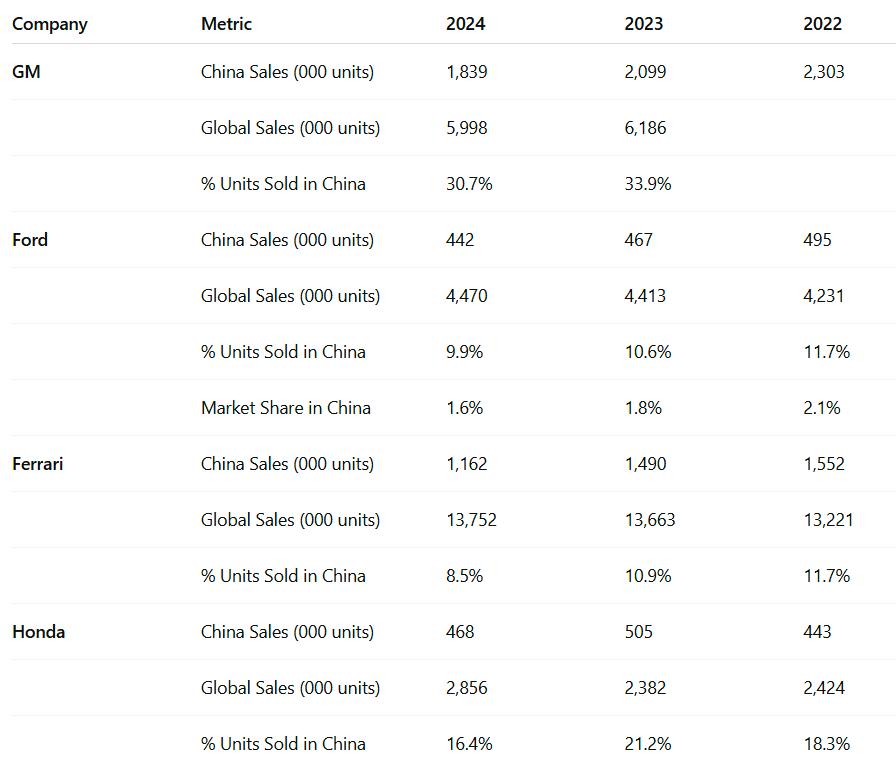

To understand the extent of the damage, which the market may not yet be discounting, I turned to Portrait. I started by asking Portrait how much China exposure each major auto manufacturer holds. Specifically, I ran the following query:

With foreign automakers losing share to domestic producers in China, I am looking to understand each company's exposure to the Chinese market.

Please create a table comparing each company's sales to China. In the table, include absolute sales (in units), percentage of units sold in China, and market share in China. Show the data for each of the past three years.

To calculate percentage of units sold in China, first locate and record the number of unit sales to China. Then, find each company's total units sold for the same period. Divide the number of units sold in China by the total units sold in the period.

From the data, the challenges are evident. Both General Motors and Ford have experienced a steady decline in China sales and market share over the past three years. General Motors, in particular, stands out - with nearly one-third of its global sales coming from China in 2024, down from previous years. This heavy dependence means that GM remains especially exposed to any ongoing weakness in the Chinese market.

To explore this theme even further, I then asked Portrait the following question for GM specifically, “To what extent are analysts concerned / covering GM's sales decline to China? Is this risk heavily priced in, or largely ignored?”

Analyst Concerns Regarding GM's China Sales Decline

Historical Context and Sales Trajectory

General Motors has experienced a prolonged and significant decline in its China business. Once a crown jewel in GM's global portfolio, the company's China operations have deteriorated substantially over recent years. GM's annual sales in China have fallen for eight consecutive years from a peak of 4.04 million units in 2017 (Web - Research - GM.UP). This decline has accelerated in recent periods, with SAIC-GM (GM's passenger-vehicle joint venture with SAIC Motor Corp) reporting a substantial 23% decline in deliveries for 2024, with only 673,007 Cadillac, Chevrolet, and Buick vehicles sold (Web - Research - GM.UP).

The market share erosion has been equally concerning. GM's share in China peaked at approximately 15% in 2017 and has fallen every year since, recently dropping to about 7% (General Motors Company Presents at J.P. Morgan Auto Conference 2024, Aug-08-2024 11:00 AM). The most recent quarterly data confirms this downward trajectory:

Q3 2024: China deliveries fell to 426K units, down 21.4% from 542K in Q3 2023, with market share dropping to 6.5% from 8.3% (General Motors Company, Q3 2024 Earnings Call, Oct 22, 2024)

Full year 2024: China deliveries fell to 1,839K units from 2,099K units in 2023, a 12.4% year-over-year decline, with market share eroding from 8.4% to 6.9% (General Motors Company, Q4 2024 Earnings Call, Jan 28, 2025)

Financial Impact and Impairment Charges

The financial consequences of GM's China sales decline have been substantial and have increasingly captured analyst attention. At its peak, GM's Chinese business contributed up to $2 billion in annual profit (Web - Research - GM.UP), but this profit engine has now reversed:

Q2 2024: GM China Auto JV reported an equity income loss of $(0.1)B, compared to a $0.1B profit in Q2 2023 (General Motors Company, Q2 2024 Earnings Call, Jul 23, 2024)

Q3 2024: GM China Auto JV reported a $0.1B loss, compared to a $0.2B profit in Q3 2023 (General Motors Company, Q3 2024 Earnings Call, Oct 22, 2024)

Full year 2024: China equity income created an $0.8B headwind to GM's overall EBIT-adjusted performance (General Motors Company, Q4 2024 Earnings Call, Jan 28, 2025)

The most significant indicator of analyst concern came in December 2024, when GM announced a massive $4.1 billion special item in auto China equity income, with approximately half related to impairment and the rest connected to restructuring actions (GM 8-K 12/02/24 Material Impairments). This included a $2.1B "other-than-temporary impairment" and $2.0B in restructuring charges in Q4 2024 (General Motors Company, Q4 2024 Earnings Call, Jan 28, 2025). GM Financial also took an impairment charge to "write down SAIC-GMAC equity investment to fair value" (General Motors Company, Q4 2024 Earnings Call, Jan 28, 2025).

The magnitude of these charges indicates that both management and analysts view the China challenges as structural rather than cyclical, requiring substantial write-downs of asset values.

Management Acknowledgment and Response

GM's management has increasingly acknowledged the severity of the China situation in their communications with investors. In every forward-looking statement section of their presentations, GM explicitly identifies China as a specific risk factor: "our business in China, which is subject to unique operational, competitive, regulatory and economic risks" (General Motors Company - Analyst/Investor Day).

CEO Mary Barra has been increasingly direct about the challenges:

Q2 2024: "Next, I'd like to discuss our results in China. As you know, the market has significant excess capacity. And many startups and established competitors continue to prioritize production over profitability... But it's clear the steps we have taken, while significant, have not been enough. We had expected to return to profitability in China in the second quarter. However, we reported a loss, and we expect the rest of the year will remain challenging because the headwinds are not easy." (General Motors Company, Q2 2024 Earnings Call, Jul 23, 2024)

Q3 2024: "However, the operating environment in China continues to be challenging, and there is more hard work to do with our partner." (General Motors Company, Q3 2024 Earnings Call, Oct 22, 2024)

In response to these challenges, GM has implemented significant restructuring actions:

Plant closures and portfolio optimization (GM 8-K 12/02/24 Material Impairments)

Reducing dealer inventory by more than 50% since the start of 2024 (General Motors Company, Q3 2024 Earnings Call, Oct 22, 2024)

Focusing on driving dealer engagement and discipline on fixed costs, inventory, pricing, and incentives (General Motors Company, Q3 2024 Earnings Call, Oct 22, 2024)

Shifting to a higher mix of new energy vehicles, which outsold ICE models for the first time in Q3 2024 (General Motors Company, Q3 2024 Earnings Call, Oct 22, 2024)

Analyst Concerns and Market Reaction

Analyst concerns about GM's China operations have evolved from cautious monitoring to explicit acknowledgment as a material headwind. The trajectory of analyst commentary reveals increasing focus on this issue:

August 2024: CFO Paul Jacobson attempted to downplay concerns, stating: "I don't necessarily accept the notion that we're struggling to make money there." (General Motors Company Presents at J.P. Morgan Auto Conference 2024, Aug-08-2024 11:00 AM)

October 2024: Despite "generally upbeat" reactions to Q2 results, analysts began explicitly mentioning China as a concern. RBC Capital Markets analyst Tom Narayan noted that "management's cautious stance on China may have weighed on the stock," while Barclays analyst Dan Levy called out "weak China ops and Cruise as main headwinds." (News - October 2024 - GM.UP)

December 2024: When GM announced the $4.1B impairment charge, analyst sentiment was "positive as should set up equity earnings improvement in 2025, but concerns around bigger than expected charge" were noted. Reuters explicitly stated that "GM's China division, once a profit engine for the Detroit company, is now losing money." (News - December 2024 - GM.UP)

The market's reaction to GM's China challenges is reflected in the company's valuation metrics. As of July 2024, GM's NTM P/E was 4.8x versus a five-year average of 7.0x, and its EV/EBITDA was 2.5x versus a five-year average of 3.0x (News - October 2024 - GM.UP). This compression in valuation multiples suggests the market has incorporated China concerns into GM's stock price to some degree.

Strategic Pivot Away from China

GM's strategic communications increasingly suggest a pivot away from China dependence toward North American operations and the EV transition. This is evident in several ways:

Limited discussion of China-specific strategies in investor presentations, despite acknowledging it as a risk factor (General Motors Company - Analyst/Investor Day)

Emphasis on North American manufacturing capabilities and EV transition strategy (General Motors Company - Analyst/Investor Day)

Focus on partnerships with Korean companies (LG Energy Solution and Samsung SDI) rather than Chinese battery manufacturers (General Motors Company - Analyst/Investor Day)

Development of a multi-supplier approach indicating efforts to build resilience against market-specific disruptions (General Motors Company - Analyst/Investor Day)

Increasing emphasis on the premium import channel as "a very capital-light way to participate in the market" (General Motors Company, Q3 2024 Earnings Call, Oct 22, 2024)

Is the China Risk Priced In?

The evidence suggests that GM's China sales decline is a significant concern for analysts that is substantially, but perhaps not fully, priced into the stock.

Evidence that the risk IS substantially priced in:

The explicit quantification of financial impacts (e.g., $0.8B negative impact on 2024 EBIT) indicates analysts are fully aware of the near-term financial implications (General Motors Company, Q4 2024 Earnings Call, Jan 28, 2025)

The massive restructuring charges and impairments ($4.1B total) suggest the company has taken a "kitchen sink" approach to address the issue comprehensively (GM 8-K 12/02/24 Material Impairments)

Management's emphasis on returning to profitability in Q4 2024 (before charges) and expectations for 2025 improvement suggest they're trying to shift the narrative from "declining business" to "turnaround story" (General Motors Company, Q4 2024 Earnings Call, Jan 28, 2025)

The fact that China is mentioned as a 2025 tailwind in guidance indicates analysts have likely already factored in the negative China performance into their models (General Motors Company, Q4 2024 Earnings Call, Jan 28, 2025)

GM's compressed valuation multiples (NTM P/E at 4.8x vs five-year average of 7.0x as of July 2024) suggest the market has incorporated these concerns to some degree (News - October 2024 - GM.UP)

Evidence that the risk may NOT be fully priced in:

The limited detailed discussion of China challenges in investor presentations suggests potential downplaying of the issue (General Motors Company - Analyst/Investor Day)

Management's relatively brief commentary on China issues in earnings calls, often focusing more on external factors than internal strategic failures (General Motors Company, Q2 2024 Earnings Call, Jul 23, 2024)

The emphasis on strong North American performance potentially masks the severity of China concerns (General Motors Company, Q3 2024 Earnings Call, Oct 22, 2024)

The absence of a comprehensive, publicly articulated China strategy beyond general restructuring actions may indicate unresolved strategic questions (General Motors Company - Analyst/Investor Day)

The full impact of China's competitive dynamics on GM's long-term global strategy and profitability may still be evolving and difficult for analysts to fully quantify

Conclusion

Analysts are increasingly concerned about GM's sales decline in China, as evidenced by explicit mentions in research notes, questions during earnings calls, and the market's reaction to the substantial impairment charges announced in December 2024. The risk appears to be substantially priced into GM's stock, as reflected in compressed valuation multiples and the positive reaction to the company's "kitchen sink" approach to restructuring.

However, the risk may not be fully priced in due to the evolving nature of the challenge, the limited detailed discussion in investor presentations, and the absence of a comprehensive, publicly articulated China strategy beyond general restructuring actions. Management's emphasis on North American strength and the EV transition may also be partially masking the full strategic implications of GM's diminished position in what was once a key growth market.

The company's strategic pivot toward North American operations, EV transition, and a more capital-light approach to the Chinese market suggests that both management and analysts recognize that GM's role in China has fundamentally changed from a growth driver to a challenging market requiring significant restructuring to achieve even modest profitability.

From the results, we find arguments both for and against the argument that GM’s China decline is already “priced in.” Certainly, a sharp analyst is already aware of the company’s struggles in the world’s second biggest economy. Nonetheless, whether the extent of the damage and future outlook is fully reflected in markets is up to interpretation, and Portrait helps provide the background and tools to explore any issue – and its market reaction – in depth.

To learn more about General Motors, the auto industry, or any other public company, head over to Portrait!