Welcome to this week's edition of the Portrait Weekly Framing. Today, we'll be analyzing McDonald's shift in pricing strategy and what it signals for the broader quick-service restaurant sector's margin trajectory.

McDonald's announcement that it will reduce prices on eight popular combo meals by 15% starting September 2025 represents more than a tactical adjustment to win back value-conscious consumers. The move, which required McDonald's corporate to offer financial subsidies to convince franchisees to accept lower margins, signals a potential inflection point for an industry that has relied on aggressive price increases to offset inflation since 2021. The burger giant's capitulation on pricing—after Big Mac combo meals reached $18.99 in some locations compared to $5.69 at the low end—suggests that even the most powerful brands in quick-service restaurants have reached the limits of consumer price tolerance.

The implications extend far beyond McDonald's 14,000 U.S. locations. With restaurant traffic down 2.7% year-to-date for fast-food establishments according to Black Box Intelligence, McDonald's pricing reset could trigger a competitive response across the sector. The company's decision to mandate that franchisees maintain combo meal prices at 15% below the sum of individual items through early 2026, up from the current 10.4% average discount, effectively establishes a new pricing benchmark that competitors will need to match or risk further traffic losses.

To understand the full implications of McDonald's pricing strategy and its potential ripple effects across the quick-service restaurant landscape, I used Portrait to analyze pricing trends and margin impacts across major QSR chains. Specifically, I ran the following Deep Research query:

Tickers: MCD, YUM, QSR, WEN, DPZ

Query: Analyze pricing strategies, same-store sales trends, and operating margin impacts across major QSR chains over the last 4 quarters through Q2 2025. Focus on how each company has balanced price increases against traffic declines, their value menu strategies, and management commentary on consumer price sensitivity. Include specific data on menu price changes, traffic trends, and margin performance.

The analysis revealed a striking pattern across the industry: while McDonald's maintained relatively stable consolidated margins through its franchise model, every major QSR chain faced intensifying pressure from the fundamental trade-off between pricing power and traffic retention. The data shows that companies attempting to maintain margins through aggressive pricing universally experienced traffic declines, with Wendy's serving as the cautionary tale—its U.S. same-store sales plummeted from positive 4.1% in Q4 2024 to negative 3.6% by Q2 2025 as consumers rejected its pricing despite management's insistence that its $5 Biggie Bag represented "the best value offering in the business."

Key Industry Themes (Q3 2024 - Q2 2025)

The Bifurcated Consumer: A persistent theme across management commentary was the divided consumer landscape. High-income households remained resilient, while low-income cohorts (often defined as those earning under $75,000) significantly pulled back on spending, choosing to eat at home more frequently (McDonald's Corporation, Q3 2024 Earnings Call, Oct 29, 2024, The Wendy's Company, Q1 2025 Earnings Call, May 01, 2025). By Q1 2025, this pressure began extending to middle-income consumers, broadening the challenge for QSRs (McDonald's Corporation, Q1 2025 Earnings Call, May 01, 2025).

The Value Imperative: In this environment, a clear and compelling value message became paramount. Brands that successfully deployed multi-layered value platforms—combining entry-level price points, meal bundles, and digital-exclusive offers—generally outperformed. McDonald's pivot to its $5 Meal Deal and Wendy's reliance on its Biggie Bag platform are prime examples of this strategic necessity (McDonald's Corporation, Q3 2024 Earnings Call, Oct 29, 2024, The Wendy's Company, Q2 2025 Earnings Call, Aug 08, 2025). However, success was not guaranteed, as Pizza Hut's struggles demonstrated that an "insufficient value message" could lead to significant market share loss (Yum! Brands, Inc., Q2 2025 Earnings Call, Aug 05, 2025).

Price vs. Traffic Trade-Off: Most operators took price throughout the period to combat commodity and labor inflation. However, the ability to do so without shedding traffic was the key differentiator. Brands like Wendy's experienced sharp traffic declines as pricing failed to hold (WEN.UR 10-Q Q2 2025), while Taco Bell successfully balanced innovation and tiered value to drive both check and positive transaction growth (Yum! Brands, Inc., Q1 2025 Earnings Call, Apr 30, 2025).

Margin Headwinds: Companies faced persistent pressure from commodity inflation (particularly beef) and elevated labor costs, especially in markets like California (Restaurant Brands International Inc., Q2 2025 Earnings Call, Aug 07, 2025, Domino's Pizza, Inc., Q1 2025 Earnings Call, Apr 28, 2025). Sales deleveraging from traffic declines exacerbated margin pressure for underperforming brands, while productivity initiatives and procurement efficiencies were key offsets for others (The Wendy's Company, Q1 2025 Earnings Call, May 01, 2025, Domino's Pizza, Inc., Q3 2024 Earnings Call, Oct 10, 2024).

McDonald's Corporation (MCD)

McDonald's navigated a volatile year, beginning with an admission that its value leadership had eroded before aggressively reasserting its affordability credentials. After a self-described "low point" in Q1 2025, the company's strategy of pairing national value deals with large-scale marketing campaigns began to yield improved results, though traffic from low-income consumers remains a significant industry-wide headwind.

Pricing and Value Strategy: McDonald's strategy evolved from reactive to proactive over the period. In Q3 2024, management acknowledged a shrinking value leadership gap and responded with the $5 Meal Deal in the U.S., which successfully drove traffic from low-income consumers and was extended through the end of the year (McDonald's Corporation, Q3 2024 Earnings Call, Oct 29, 2024). This culminated in the January 2025 launch of the formal McValue platform, which included the $5 meal and a "buy 1 add 1 for a dollar" offer (McDonald's Corporation, Q1 2025 Earnings Call, May 01, 2025). While the $5 deal performed well, by Q2 2025 management emphasized that the most significant driver of consumer value perception is core menu pricing, signaling a system-wide focus on franchisee pricing to improve affordability at the local level (McDonald's Corporation, Q2 2025 Earnings Call, Aug 06, 2025). This was complemented by innovation like Snack Wraps at a $2.99 price point to broaden the value spectrum (McDonald's Corporation, Q2 2025 Earnings Call, Aug 06, 2025).

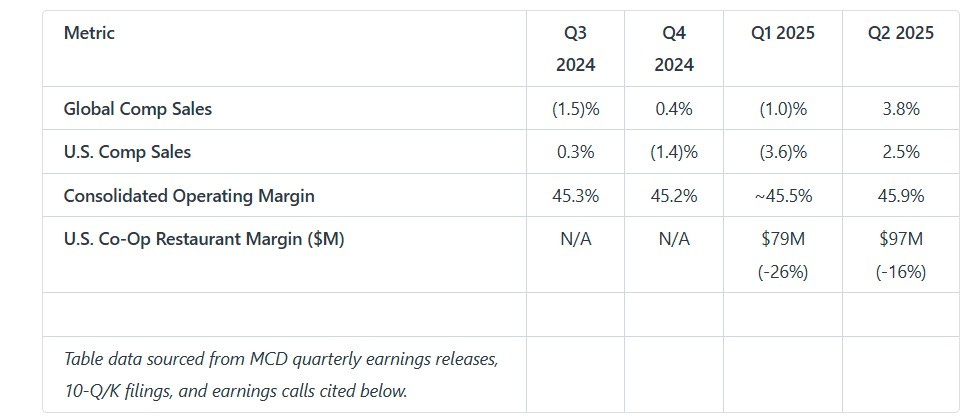

Same-Store Sales and Traffic: Performance was uneven, bottoming out in early 2025. U.S. comps were slightly positive in Q3 2024 (+0.3%) on check growth, but with negative guest counts (MCD 10-Q Q3 2024). Q4 2024 U.S. comps fell 1.4%, heavily impacted by an E. coli outbreak, though underlying guest counts were slightly positive, suggesting the value message was gaining traction (McDonald's Corporation, Q4 2024 Earnings Call, Feb 10, 2025). Q1 2025 was the nadir, with U.S. comps falling 3.6% as negative traffic from both low- and middle-income consumers intensified (McDonald's Corporation, Q1 2025 Earnings Call, May 01, 2025). A significant rebound occurred in Q2 2025, with U.S. comps up 2.5% and global comps up 3.8%, driven by the combination of the value platform and the global Minecraft movie marketing campaign, which boosted guest counts (McDonald's Corporation, Q2 2025 Earnings Call, Aug 06, 2025).

Operating Margin Impact: The company's highly franchised model provided consolidated margin stability, with the adjusted operating margin remaining in the mid-40% range throughout the period (MCD 8-K 10/29/24 Earnings Release, MCD.UP 10-Q Q2 2025). However, company-operated stores faced significant pressure. In Q1 2025, U.S. company-owned restaurant margins fell 26% to $79 million, and in Q2 2025 they fell another 16% to $97 million, reflecting weak top-line results, commodity inflation, and wage pressures (MCD.UP 10-Q Q1 2025, MCD.UP 10-Q Q2 2025). This forced management to lower its full-year 2025 margin outlook for company-operated restaurants to be flat with 2024's 14.8% level, down from a prior expectation of a slight increase (McDonald's Corporation, Q2 2025 Earnings Call, Aug 06, 2025).

Yum! Brands (YUM)

Yum! Brands' performance was a tale of three distinct businesses. Taco Bell was the undisputed growth engine, consistently gaining market share through a masterful blend of value and innovation. KFC's results were bifurcated, with solid international growth masking persistent value and operational challenges in the U.S. Pizza Hut remained the primary drag on performance, struggling to establish a compelling value proposition in a highly competitive domestic market.

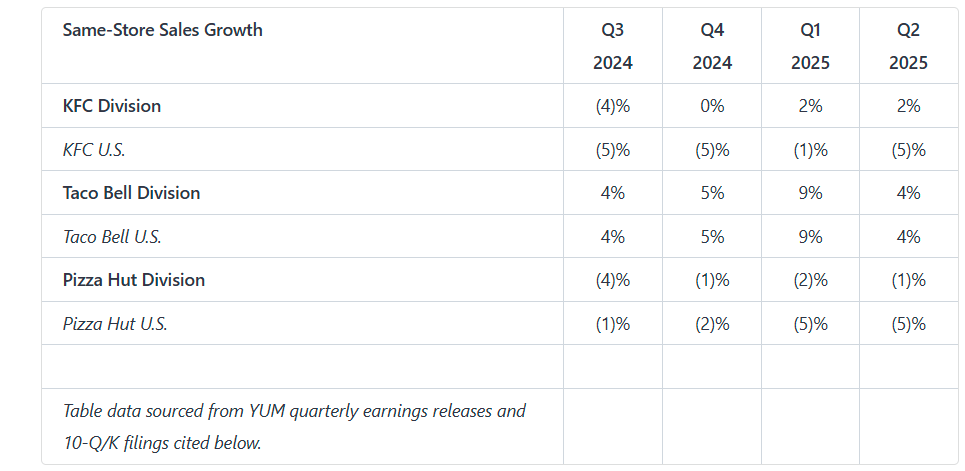

Taco Bell: The brand was a standout performer, consistently outpacing the industry. U.S. SSS growth was strong and steady, peaking at an exceptional +9% in Q1 2025 (YUM 8-K 04/30/25 Earnings Release). Its success was rooted in a multi-tiered strategy that appealed to all income cohorts. The Cravings Value Menu, alongside compelling $5, $7, and $9 Luxe Box offerings, provided accessible entry points, while culturally relevant innovations like the Crispy Chicken Taco drove excitement and check growth (Yum! Brands, Inc., Q1 2025 Earnings Call, Apr 30, 2025, Yum! Brands, Inc., Q2 2025 Earnings Call, Aug 05, 2025). This strategy drove positive transaction growth and market share gains, with management noting in Q2 2025 that the brand was capturing trade-down from fast-casual (Yum! Brands, Inc., Q2 2025 Earnings Call, Aug 05, 2025). Company restaurant margins remained robust, generally in the 22-25% range, though they faced some pressure from commodity and labor inflation (YUM 10-Q Q1 2025, YUM.UP 10-Q Q2 2025).

KFC: The division's results masked significant underlying weakness in its U.S. business. U.S. SSS declined 5% in three of the last four quarters (YUM 8-K 11/05/24 Earnings Release, YUM 8-K 02/06/25 Earnings Release, YUM 8-K 08/05/25 Earnings Release). Management explicitly acknowledged "gaps in value perception" and inconsistent consumer experiences in the U.S. (Yum! Brands, Inc., Q2 2025 Earnings Call, Aug 05, 2025). While value promotions like $5 bowls drove some transaction growth in Q1 2025, the brand is now embarking on a "Kentucky Fried comeback" campaign to address these core issues (Yum! Brands, Inc., Q1 2025 Earnings Call, Apr 30, 2025). In contrast, international markets were generally positive, with strength in the U.K., Africa, and Latin America often driven by a sharper focus on value offerings in the €3 to €5 range (Yum! Brands, Inc., Q4 2024 Earnings Call, Feb 06, 2025, Yum! Brands, Inc., Q2 2025 Earnings Call, Aug 05, 2025).

Pizza Hut: The division consistently underperformed, particularly in the U.S., where SSS declined 5% in both Q1 and Q2 2025 (YUM 8-K 04/30/25 Earnings Release, YUM 8-K 08/05/25 Earnings Release). Management repeatedly stated that the brand's value message was insufficient to compete against deep value offers in the market (Yum! Brands, Inc., Q3 2024 Earnings Call, Nov 05, 2024, Yum! Brands, Inc., Q2 2025 Earnings Call, Aug 05, 2025). While innovations like Cheesy Bites and the Chicago Tavern Style Pizza resonated with existing customers, they failed to drive new traffic. The brand is now pivoting to more explicit value offers like "Wing Wednesday" to regain traction (Yum! Brands, Inc., Q2 2025 Earnings Call, Aug 05, 2025). The poor sales performance, combined with higher bad debt expense from franchisee transitions, led to significant declines in divisional operating profit, which fell 18% in Q1 and 15% in Q2 2025 (YUM 10-Q Q1 2025, YUM.UP 10-Q Q2 2025).

Wendy's (WEN)

Wendy's experienced a dramatic and rapid deterioration in performance over the past year. After a promotional high in late 2024, the company faced a severe consumer pullback in the first half of 2025, leading to sharp traffic declines, underperformance in its key breakfast daypart, and two significant downward revisions to its full-year guidance. The challenges were compounded by high-level executive turnover, underscoring the depth of the operational and strategic issues.

Pricing and Value Strategy: Wendy's strategy centered on its Biggie Bag platform, which management consistently referred to as a core value proposition (The Wendy's Company, Q3 2024 Earnings Call, Oct 31, 2024). However, the platform's effectiveness waned as consumer pressure mounted. The standout success was the Q4 2024 SpongeBob promotion, which drove a 20% sales lift at its peak and fueled a 4.1% SSS gain (The Wendy's Company, Q4 2024 Earnings Call, Feb 13, 2025). This success proved fleeting. As the consumer environment weakened in 2025, the company's innovation efforts, such as a Takis collaboration, underperformed expectations (The Wendy's Company, Q2 2025 Earnings Call, Aug 08, 2025). Despite management calling the $5 Biggie Bag the "best value offering in the business," the persistent and accelerating traffic declines suggest this message failed to overcome competitive value offerings or consumer reticence (The Wendy's Company, Q2 2025 Earnings Call, Aug 08, 2025).

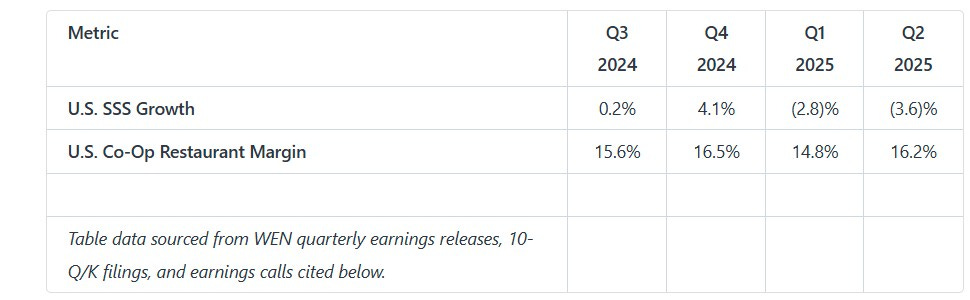

Same-Store Sales and Traffic: The trend was one of sharp decline. After nearly flat U.S. SSS in Q3 2024 (+0.2%) and the promotional surge in Q4 2024 (+4.1%), performance fell off a cliff (WEN 10-Q Q3 2024, The Wendy's Company, Q4 2024 Earnings Call, Feb 13, 2025). U.S. SSS dropped 2.8% in Q1 2025 and worsened to a 3.6% decline in Q2 2025, both driven by significant decreases in customer traffic (WEN 8-K 05/02/25 Earnings Release, WEN.UR 10-Q Q2 2025). Management attributed the weakness to a "weaker-than-expected consumer environment," particularly among households earning under $75,000 (The Wendy's Company, Q1 2025 Earnings Call, May 01, 2025). The negative momentum was so severe that management disclosed July 2025 comps were down 5% to 6%, forcing a drastic cut in the full-year global systemwide sales outlook to a decline of 3% to 5% (The Wendy's Company, Q2 2025 Earnings Call, Aug 08, 2025).

Operating Margin Impact: Margins eroded under the pressure of sales deleveraging and rising costs. After a strong Q4 2024 where margin expanded 300 bps to 16.5% on strong sales leverage, the trend reversed (WEN 8-K 02/13/25 Earnings Release). U.S. company-operated restaurant margin contracted to 14.8% in Q1 and 16.2% in Q2, pressured by traffic declines, wage inflation, and rising commodity costs (WEN 8-K 05/02/25 Earnings Release, WEN.UR 8-K 08/08/25 Earnings Release). The company twice raised its full-year commodity inflation outlook, from 1% initially to 2.5% in Q1, and then to 4% in Q2, citing beef prices (The Wendy's Company, Q1 2025 Earnings Call, May 01, 2025, The Wendy's Company, Q2 2025 Earnings Call, Aug 08, 2025). Consequently, the full-year U.S. company-operated margin outlook was cut to 14% +/- 50 bps, down significantly from the initial guidance of ~16% (The Wendy's Company, Q2 2025 Earnings Call, Aug 08, 2025).

Domino's Pizza, Inc. (DPZ)

Domino's executed a strategy focused on "renowned value," operational execution, and product innovation. The company successfully navigated a bifurcation in its business, with a robust carryout segment offsetting persistent pressure on its delivery channel. The strategic expansion into third-party aggregator marketplaces and a highly successful product launch in Q2 2025 enabled the company to reverse negative traffic trends and accelerate sales growth, all while delivering consistent margin expansion through supply chain efficiencies.

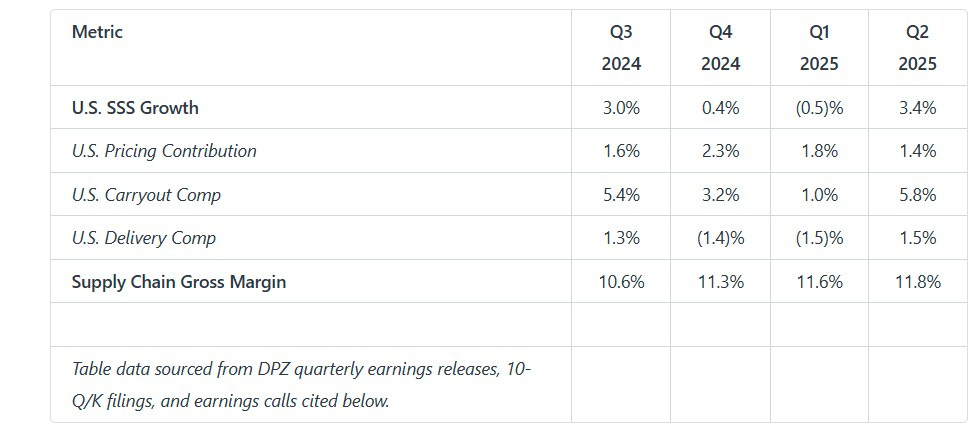

Pricing and Value Strategy: Domino's maintained a disciplined pricing approach, with price contributing a modest 1.4% to 2.3% to U.S. SSS each quarter (Domino's Pizza, Inc., Q3 2024 Earnings Call, Oct 10, 2024, Domino's Pizza, Inc., Q2 2025 Earnings Call, Jul 21, 2025). The core value strategy was multifaceted, relying on the revamped Domino's Rewards program, which drove carryout traffic, and national promotions like the "best deal ever" (Domino's Pizza, Inc., Q3 2024 Earnings Call, Oct 10, 2024, Domino's Pizza, Inc., Q1 2025 Earnings Call, Apr 28, 2025). The most impactful strategic move was the Q2 2025 launch of Parmesan Stuffed Crust. This premium innovation, which carried a ~$4 upcharge on the Mix & Match platform, successfully drove both ticket and profit without resorting to deep discounting (Domino's Pizza, Inc., Q2 2025 Earnings Call, Jul 21, 2025). The company also expanded its reach by completing its national rollout with DoorDash, setting the stage for incremental sales in the second half of 2025 (Domino's Pizza, Inc., Q2 2025 Earnings Call, Jul 21, 2025).

Same-Store Sales and Traffic: Performance inflected positively in Q2 2025. After a solid Q3 2024 (+3.0% U.S. SSS) with positive order counts, growth decelerated to +0.4% in Q4 2024 and turned negative at -0.5% in Q1 2025, driven by negative traffic (Domino's Pizza, Inc., Q3 2024 Earnings Call, Oct 10, 2024, DPZ 8-K 02/24/25 Earnings Release, DPZ 10-Q Q1 2025). Management attributed the weakness to macro pressure on low-income consumers, which disproportionately impacted the delivery business (-1.4% in Q4, -1.5% in Q1) (Domino's Pizza, Inc., Q4 2024 Earnings Call, Feb 24, 2025, Domino's Pizza, Inc., Q1 2025 Earnings Call, Apr 28, 2025). The carryout segment remained a consistent source of strength. The Parmesan Stuffed Crust launch in Q2 2025 reversed the trend, propelling U.S. SSS to +3.4% on the back of positive transaction counts, with carryout comps surging +5.8% and delivery returning to positive growth at +1.5% (Domino's Pizza, Inc., Q2 2025 Earnings Call, Jul 21, 2025).

Operating Margin Impact: A key pillar of Domino's profit growth was the consistent expansion of its supply chain gross margin, which grew from 10.6% in Q3 2024 to 11.8% by Q2 2025 (DPZ 10-Q Q3 2024, DPZ.UR 8-K 07/21/25 Earnings Release). This was consistently attributed to procurement productivity initiatives, which helped drive operating income growth throughout the period. For example, in Q2 2025, income from operations increased 14.9% (ex-FX), supported by higher franchise royalties from strong SSS and gross margin dollar growth in the supply chain (Domino's Pizza, Inc., Q2 2025 Earnings Call, Jul 21, 2025).

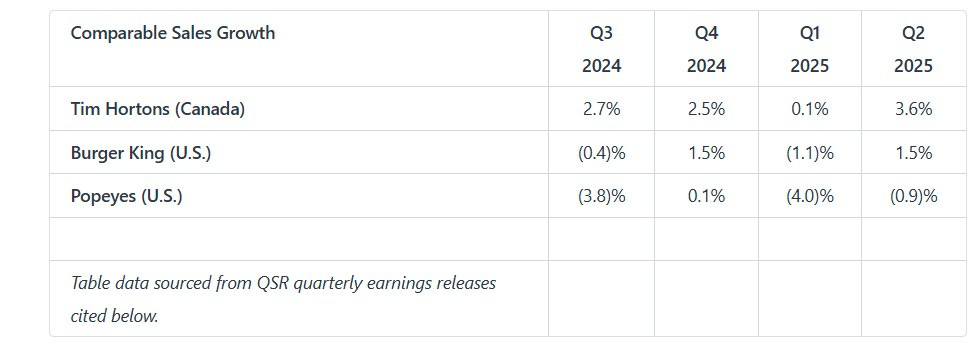

Restaurant Brands International (QSR)

QSR's portfolio showed divergent results. Tim Hortons was a model of consistency, leveraging its strong position in Canada to drive steady, traffic-led growth. Burger King's U.S. turnaround under the "Reclaim the Flame" initiative showed encouraging but uneven progress, outperforming peers but still posting negative comps in two of the four quarters. Popeyes struggled with its value message in a difficult environment, leading to negative U.S. comps and a strategic pivot toward affordability and operational simplicity.

Tim Hortons: The Canadian brand was a consistent traffic driver. It posted 15 consecutive quarters of positive traffic growth through Q4 2024 (Restaurant Brands International Inc., Q4 2024 Earnings Call, Feb 12, 2025). Its strategy successfully balanced value, such as a "$3 hot breakfast sandwich" offer, with innovation in cold beverages and PM foods like Flatbread Pizza, which carried a higher average check (Restaurant Brands International Inc., Q3 2024 Earnings Call, Nov 05, 2024). Even in a soft Q1 2025 (+0.1% comp), the brand rebounded strongly in Q2 (+3.6% comp) driven by a balanced contribution from check and traffic, highlighting the resilience of its business model and market position (Restaurant Brands International Inc., Q2 2025 Earnings Call, Aug 07, 2025).

Burger King (U.S.): The brand's performance was choppy but showed signs of progress. After a soft Q3 2024 (-0.4% comp), a focus on core equities like the Whopper and effective marketing led to a +1.5% comp in Q4 2024, outperforming peers (Restaurant Brands International Inc., Q4 2024 Earnings Call, Feb 12, 2025). Performance dipped again in Q1 2025 (-1.1% comp) amid macro pressures but rebounded to +1.5% in Q2 2025 (QSR 8-K 05/08/25 Earnings Release, QSR.UP 8-K 08/07/25 Earnings Release). The strategy involved balancing value offerings like "$5 Duos and $7 Trios" with premium innovation, while stabilizing the percentage of sales on deal to pre-pandemic levels (Restaurant Brands International Inc., Q1 2025 Earnings Call, May 08, 2025, Restaurant Brands International Inc., Q2 2025 Earnings Call, Aug 07, 2025). Margin impact was notable from the fall-off of corporate "Fuel the Flame" ad contributions and rising beef prices, which were up high-teens YoY in H1 2025 (Restaurant Brands International Inc., Q2 2025 Earnings Call, Aug 07, 2025).

Popeyes (U.S.): The brand struggled significantly with its value proposition. A sharp -3.8% comp in Q3 2024 was attributed to a marketing calendar that was "missing some of the offers consumers were looking for" in a value-sensitive environment (Restaurant Brands International Inc., Q3 2024 Earnings Call, Nov 05, 2024). This prompted a pivot to more explicit value, including a "3 pieces of chicken for $5" offer and a "$6 big box", which helped stabilize comps to +0.1% in Q4 2024 (Restaurant Brands International Inc., Q3 2024 Earnings Call, Nov 05, 2024, QSR 8-K 02/12/25 Earnings Release). However, the brand lapsed a strong prior-year comparison in Q1 2025, with comps falling 4.0%, and they remained negative at -0.9% in Q2 2025 (QSR 8-K 05/08/25 Earnings Release, QSR.UP 8-K 08/07/25 Earnings Release). The "Easy to Love" turnaround plan, which includes higher franchisee ad contributions, is now in place to address these issues (Restaurant Brands International Inc., Q4 2024 Earnings Call, Feb 12, 2025).

The analysis reveals that the QSR sector has entered a new phase where the post-pandemic pricing playbook no longer works. Companies that relied on price increases to offset inflation without investing in compelling value platforms have seen dramatic traffic erosion, while those that balanced innovation with value messaging have maintained momentum. As McDonald's CEO Chris Kempczinski noted, "the single biggest driver of what shapes a consumer's overall perception of McDonald's value is the menu board"—a reality that applies equally to every competitor in the space.

Looking forward, the winners in this environment will likely be companies with the operational flexibility to absorb margin pressure while maintaining traffic, the innovation capabilities to drive mix without relying solely on price, and the financial strength to invest in value messaging when competitors are retrenching. McDonald's decision to subsidize franchisees represents a bet that traffic recovery will ultimately drive operating leverage that more than offsets near-term margin compression—a bet that the entire industry will be watching closely as the new pricing regime takes effect in September 2025.

To further research McDonald's, Wendy's, Yum Brands, or other quick-service restaurant companies navigating this pricing reset, head over to Portrait today!